Navigating the personal loan application process may seem daunting, but with the right knowledge and preparation, you can make it a straightforward and empowering experience.

Whether you’re looking to consolidate debt, fund a major purchase, or cover an unexpected expense, Understanding the intricacies of personal loan applications is crucial for securing the best terms and avoiding potential pitfalls.

In this comprehensive guide, we’ll take you through the essential steps, considerations, and frequently asked questions surrounding the personal loan application process. From assessing your financial health to selecting the appropriate loan type and managing post-approval responsibilities, we have you covered.

Assessing Your Financial Health Before Applying

Before you dive into the personal loans application process, it’s crucial to take a close look at your financial standing. This will not only help you determine the best loan option but also increase your chances of approval and securing favorable terms.

The Importance of Credit Scores

Your credit score is one of the primary factors lenders consider when evaluating your loan application. According to Experian, a credit score of 700 or higher is generally considered “good,” while a score of 800 or above is considered “excellent.” Lenders typically offer lower interest rates and more favorable terms to borrowers with higher credit scores.

Understanding Debt-to-Income Ratio

Another key metric lenders evaluate is your debt-to-income (DTI) ratio. This ratio compares your monthly debt payments to your monthly gross income, and a DTI of 35% or lower is generally considered ideal for loan approval. Keeping your DTI in check can significantly improve your chances of getting approved for a personal loan.

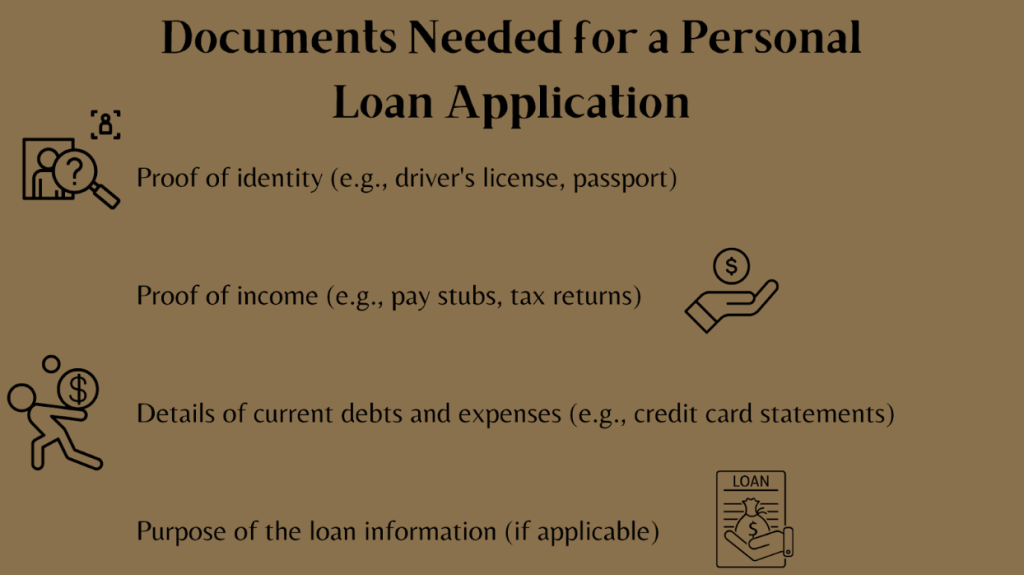

Gathering Financial Documents

Before you apply for a personal loan, make sure to have the following documents ready: proof of income (such as pay stubs, tax returns, or bank statements), identification, and any other information your lender may require. Being prepared with these materials can streamline the application process and help you avoid delays.

Check out the website to know more.

Reviewing your credit score, and debt-to-income ratio, and gathering the necessary documents ahead of time can give you a significant advantage in the personal loan application process. This preparation will not only help you identify the best loan option but also demonstrate to lenders that you are a responsible and informed borrower.

Choosing the Right Personal Loan for Your Needs

Once you’ve assessed your financial health, it’s time to explore the personal loan options and determine which one best suits your needs.

Secured vs. Unsecured Loans

Secured personal loans are backed by collateral, such as a car or home, while unsecured loans do not require any form of collateral. Secured loans typically have lower interest rates and higher loan amounts, but they come with the risk of losing your collateral if you default on the loan. Unsecured loans, on the other hand, have higher interest rates and lower loan amounts, but they don’t require you to put up any assets.

Fixed-rate vs. Variable-rate Loans

Personal loans can also come with either fixed or variable interest rates. Fixed-rate loans offer predictable monthly payments, as the interest rate remains the same throughout the loan’s lifetime. Variable-rate loans, however, have interest rates that can fluctuate based on market conditions, potentially leading to lower payments in a declining interest rate environment, but also the risk of higher payments if rates rise.

To assist you in weighing the pros and cons of each option, consider the following comparison table:

| Loan Type | Interest Rate | Loan Amount | Collateral Required | Predictability of Payments |

| Secured | Lower | Higher | Yes | Moderate |

| Unsecured | Higher | Lower | No | High |

| Fixed-rate | Stable | Varies | Varies | High |

| Variable-rate | Fluctuates | Varies | Varies | Low |

Carefully evaluate your financial situation, borrowing needs, and risk tolerance to determine which loan type best suits your needs..

Navigating the Application Process

With a clear understanding of your financial health and the different loan options available, you’re now ready to navigate the personal loan application process.

Pre-Qualification vs. Pre-Approval

Before you officially apply for a personal loan, you may want to explore the option of pre-qualification or pre-approval. Pre-qualification is an initial estimate of the loan amount and terms you may qualify for, based on a soft credit check that doesn’t impact your credit score. Pre-approval, on the other hand, is a more comprehensive process that involves a hard credit check and verification of your income and assets.

Avoiding Common Mistakes

When applying for a personal loan, it’s important to avoid common pitfalls that can hinder your chances of approval or lead to unfavorable terms. These include failing to compare offers from multiple lenders, neglecting to review the fine print, and applying for a loan that exceeds your debt-to-income ratio.

Understanding Loan Offers and Terms

Once you’ve submitted your personal loan application, it’s time to review the offers and terms carefully. This step is crucial in ensuring you get the best possible deal.

Analyzing APR, Fees, and Other Charges

When evaluating loan offers, pay close attention to the annual percentage rate (APR), which reflects the true cost of borrowing. Additionally, be mindful of any fees, such as origination fees or prepayment penalties, that may be associated with the loan.

Negotiating Better Terms

In some cases, you may be able to negotiate certain aspects of the loan offer, such as the interest rate or repayment period. However, keep in mind that the lender’s willingness to negotiate will depend on factors like your creditworthiness and the loan type.

Final Steps and Post-Application Considerations

The personal loan application process doesn’t end once you’ve accepted an offer. There are a few final steps and ongoing responsibilities to keep in mind.

What to Do If Your Loan is Rejected

If your personal loan application is rejected, don’t get discouraged. Instead, take the time to understand the reasons behind the rejection and work on improving your financial profile. This may include taking steps to boost your credit score, reducing your debt-to-income ratio, or exploring alternative loan options.

Managing Your Loan Responsibly

Once you’ve secured your personal loan, it’s crucial to manage it responsibly. This includes making timely payments, setting up automatic payments to avoid late fees, and avoiding additional borrowing that could put you at risk of falling into a debt trap. Responsible loan management can also have a positive impact on your credit score over time.

Frequently Asked Questions

- How long does the personal loan application process typically take?

The timeline for the personal loan application process can vary depending on the lender and the type of loan you’re applying for. Generally, the process can take anywhere from a few days to a few weeks, from the initial application to the final approval and funding.

- Can I apply for a personal loan if I have a bad credit score?

Yes, it is possible to apply for a personal loan even if you have a poor credit score, but your options may be more limited. Lenders may be willing to consider you if you apply for a secured loan or have a co-signer with a stronger credit profile. However, you may face higher interest rates and less favorable terms compared to borrowers with excellent credit.

- Are there any alternatives to personal loans for emergency funds?

If you need emergency funds, there are a few alternatives to personal loans to consider, such as:

- Home equity line of credit (HELOC): A HELOC allows you to borrow against the equity in your home, typically at a lower interest rate than a personal loan.

- Credit card advances: Some credit cards offer cash advance options, which can provide quick access to funds, though often with higher interest rates.

- Hardship programs: If you’re struggling with existing debts, some lenders or creditors may offer hardship payment plans or temporary relief to help you through a financial emergency.

Remember, it’s important to carefully weigh the pros and cons of each option and choose the one that best fits your specific financial situation and needs.

Conclusion

Navigating the personal loan application process can be a complex undertaking, but with the right knowledge and preparation, you can turn it into a smooth and empowering experience.

By assessing your financial health, choosing the right loan type, and managing the application and post-approval responsibilities, you’ll be well on your way to securing the personal loan that best fits your needs.

With this comprehensive guide as your reference, you’ll be equipped to navigate the personal loan landscape and achieve your financial goals.